TCS IV vs HV Chart | Volatility Premium & Discount Analysis

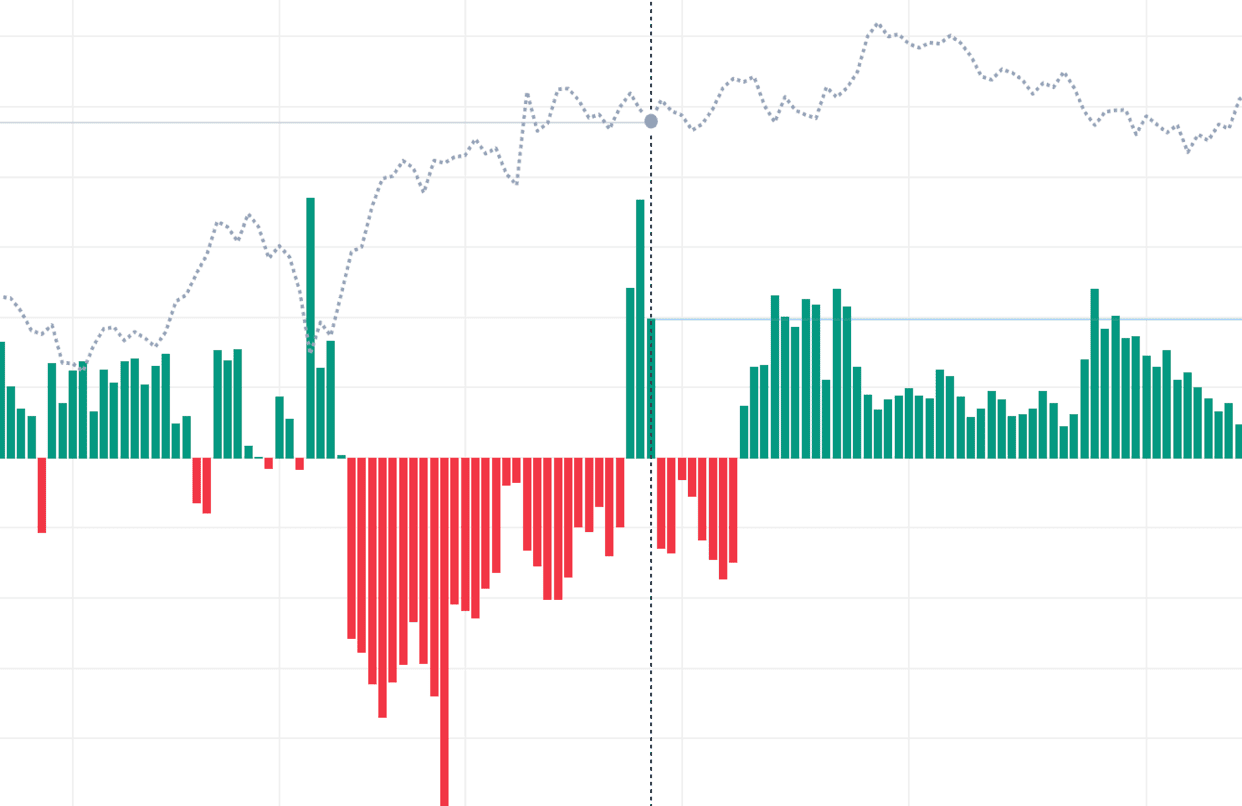

IV vs HV for TCS is the cleanest way to tell whether options on this underlying are cheap or expensive at any moment. Implied volatility (IV) is the volatility number baked into current TCS option prices — what the market expects going forward. Historical volatility (HV) is the actual standard deviation of past TCS returns over a chosen window — what the stock has actually done. The gap between the two tells you whether option buyers are over- or under-paying relative to recent reality.

When TCS IV is meaningfully above HV, the option market is pricing in more volatility than has actually been realized — premium is rich, and strategies like selling strangles, short straddles, and iron condors have favourable math. When IV drops below HV, option premium is cheap relative to the moves TCS has been making, and long-volatility strategies (long straddles, backspreads) get interesting. The ratio also reveals regime changes: a sustained IV-HV premium collapse often precedes breakouts, while expanding IV-HV premium usually marks complacency ahead of events.

Practical use of TCS IV-HV on NSE F&O

Most systematic option-selling strategies on TCS should filter entries by IV-HV gap — entering short-premium trades only when IV is sufficiently above HV compensates for the inherent tail risk. For event-day trades (budget, RBI, expiry), comparing current TCS IV with the HV you'd expect during the event window helps you decide whether the implied move is realistic, optimistic, or conservative — a crucial input for sizing and strike selection.

Combine IV vs HV with our IV Chart, Volatility Skew, and ATM Straddle Chart for a full TCS volatility analysis stack on NSE.

Tata Consultancy Services Ltd (TCS) IV-HV: Daily Routine

Morning TCS check

At market open, check the Tata Consultancy Services Ltd IV-HV chart. Note today's spread value and its direction from yesterday. Is the spread widening or contracting? Is it in a normal range or extreme? Write the numbers in your journal. This 1-minute morning check establishes your volatility context for the day.

Pre-trade check for TCS

Before entering any TCS options trade, glance at the IV-HV chart. Does the current environment support your trade idea? High spreads support short premium, low spreads support long premium. Trades that fight the IV-HV environment usually underperform. This filter is free and takes 5 seconds — always use it.

Mid-day monitoring on TCS

For active intraday traders, check the IV-HV chart every 1-2 hours during the session. Changes in the spread can signal shifts in market conditions. Rapid spread widening may warn of trouble; contraction may signal opportunities. Active monitoring catches these shifts in real time.

End-of-day journal entry as of 17 July 2026

At market close, note the final IV-HV values and any interesting patterns from the day. Over weeks this journal builds a library of your observations about Tata Consultancy Services Ltd volatility behaviour. These observations inform your future trade decisions far better than any generic guide.

Tata Consultancy Services Ltd (TCS) IV-HV Chart: Event-Driven Analysis

How events affect TCS IV-HV

Events like Tata Consultancy Services Ltd earnings and corporate actions cause IV to spike while HV stays relatively stable. The spread widens dramatically in the days before the event. After the event, IV crushes back toward HV. The chart clearly shows this pre-event widening and post-event narrowing.

Pre-event TCS trade setups

When you see the IV-HV spread widening in the days before a known event, short premium trades are setting up. IV will likely peak on or near the event date, then collapse afterward. Selling before the peak and covering after captures the crush. The risk is that direction moves sharply against you — use defined-risk structures like iron condors.

Post-event TCS trade setups

After the event resolves, IV usually drops fast. If you see IV has crushed to near HV levels (spread is normal again), the trade opportunity is over — wait for the next cycle. If IV stays elevated above HV despite the event being over, something unusual is happening — investigate before trading.

Building an event-trading routine on TCS as of 17 July 2026

Mark major event dates on your calendar. Start watching the IV-HV chart 5-7 sessions before each event. Look for widening spreads. Enter short premium trades 1-3 days before the event. Exit within 24 hours after the event resolves. This disciplined cycle produces consistent results on Tata Consultancy Services Ltd around major events.

Tata Consultancy Services Ltd (TCS) IV-HV: Common Mistakes

Mistake 1: ignoring the spread direction on TCS

A static spread number is less useful than the trend. An IV-HV spread of 5% that has been widening from 2% is very different from 5% that has been contracting from 10%. Always check the direction of movement, not just the current level. The direction is usually the more actionable signal on Tata Consultancy Services Ltd.

Mistake 2: using the wrong HV window

Short HV windows are noisy. Long windows are stale. Matching the HV window to your trade timeframe is essential. Day traders using 90-day HV are reading outdated data. Positional traders using 10-day HV are reacting to noise. Use the window that fits your holding period.

Mistake 3: assuming IV-HV trades are low risk

Even with a statistical edge, individual trades can lose. A mean-reversion setup can deepen before reverting. Events can cause unexpected spikes that damage short premium positions. Always use position sizing that allows for a few consecutive losers without breaking your account.

Mistake 4: ignoring the event calendar on TCS as of 17 July 2026

IV-HV spreads behave abnormally around events. A spread that looks extreme pre-event may be "normal" for that event type. Without checking the event calendar, you can mistake event-driven spreads for mean-reversion opportunities and lose money. Always know what is coming up on the Tata Consultancy Services Ltd calendar.

IV vs HV: Video Walkthrough

TCS IV-HV spread: quick reference

| IV minus HV (vol points) | Premium regime | Common reading |

|---|---|---|

| Below 0 | Volatility discount | Rare; options cheap vs realized moves — long straddles and backspreads favoured |

| 0 – 2 | Thin premium | Quiet regime on TCS; little edge for either side |

| 2 – 5 | Normal risk premium | Standard short-premium zone — strangles, iron condors, credit spreads |

| 5 – 10 | Event-inflated premium | Market pricing an event (results, RBI, budget); rich premium but real move risk |

| Above 10 | Extreme premium | Typical pre-earnings on stocks; expect IV crush once the event passes |

These bands are typical NSE tendencies, not fixed rules — indices usually hold a smaller IV-HV spread than single stocks, and spreads widen ahead of scheduled events. The live TCS chart above plots IV minus HV each session, so you can see which regime the option market is pricing right now and how today compares with recent history.

How to use the IV vs HV chart

- Pick an underlying — Select Nifty, BankNifty, or an F&O stock to compare implied versus historical volatility for.

- Compare the lines — IV is the forward-looking line; HV is the backward-looking line. Look at the current vertical gap between them.

- Evaluate the spread — A positive spread (IV > HV) favours premium-selling. A negative or near-zero spread favours premium-buying or long-volatility strategies.

- Check historical context — Scan how the spread has behaved over recent months. Is today's spread normal for this stock, or an outlier?

- Pick a strategy — Elevated IV-HV spread → short strangles, iron condors, credit spreads. Compressed IV-HV → long straddles, backspreads, debit spreads.

TCS IV vs HV — Frequently Asked Questions

What is TCS IV vs HV?

TCS IV (Implied Volatility) is the volatility priced into current option premiums — the market's forward expectation. HV (Historical Volatility) is the annualised standard deviation of actual past TCS returns over a chosen window. When IV is above HV, options are relatively expensive; when IV is below HV, option premium is cheap versus realized movement.

How to trade TCS using IV vs HV?

Use the TCS IV-HV spread as a strategy filter. When IV is well above HV, premium is rich — selling structures like short strangles and iron condors have favourable expected value. When IV drops to or below HV, premium is cheap — long straddles and backspreads become attractive. Always confirm with price action and upcoming events before entering.

Does TCS IV move before HV?

Yes. IV reacts the moment expectations change because it is derived from live TCS option prices, while HV only updates as new daily returns enter its rolling window, so it lags by several sessions. An IV spike ahead of an event is therefore a leading signal — by the time HV catches up, the move has usually already happened.

What is a normal IV-HV spread for TCS?

Most NSE underlyings, including TCS, trade with IV about 1-3 percentage points above HV — a normal volatility risk premium. A spread above 5 points usually signals event anticipation (results, budget, RBI policy) and tends to revert once the event passes. IV falling below HV is rare and marks unusually cheap option premium.

How often does the TCS IV vs HV chart update?

During NSE market hours (9:15 AM to 3:30 PM IST) the TCS IV line refreshes from the live option chain, while HV is recalculated from daily closing returns over your selected window (21 sessions by default). Outside market hours the chart shows the last traded session, and the historical series lets you study past spread behaviour.