TCS Implied Volatility (IV) Chart today | Live NSE Data

Track real-time and historical TCS Implied Volatility (IV) with StockMojo's advanced charting tool. Implied volatility is a critical metric for options traders, representing the market's expectation of future price movement and determining the premium price of option contracts.

Use our live TCS IV chart to identify whether options are overvalued or undervalued. Analyze IV percentile and IV rank to compare current volatility levels against historical data, helping you choose the right options strategy—whether it's buying options during low IV periods or selling premiums when IV is elevated. Our intraday IV tracking helps you spot volatility spikes and crushes around major market events and earnings announcements.

Enhance your volatility analysis with our IV Grid Screener,Volatility Skew, and Open Interest tools.

Tata Consultancy Services Ltd (TCS) IV Chart: Pre-market and End-of-Day Routine

Why a routine matters for TCS IV analysis

Consistency beats intensity. Checking the Tata Consultancy Services Ltd IV chart at fixed times every day builds pattern recognition that random checking cannot. A routine takes 5-10 minutes total per day but compounds into significant trading edge over months.

Pre-market TCS IV check

Before the market opens, note yesterday's closing IV for Tata Consultancy Services Ltd. Compare to the 5-day, 20-day, and 90-day averages. Classify today's expected regime — compression, moderate, expansion, or extreme. This framework drives your trading bias for the day.

Mid-day TCS IV check

Around midday, check whether today's live IV is tracking expectations. If it is rising faster than expected, something is up — investigate. If it is falling faster, premium is crushing and opportunities for short covering may emerge. These mid-session observations keep you aligned with actual conditions.

End-of-day TCS IV routine as of 15 July 2026

At close, note the final IV for the session. Compare to the opening value. Is IV rising, falling, or flat through the day? Write down the observation in your journal. Over weeks and months, this log becomes a personalised Tata Consultancy Services Ltd volatility playbook that no generic guide can match.

Tata Consultancy Services Ltd (TCS) IV Chart: Comparing Today to Historical Range

Why historical context matters for TCS IV

IV values without context are meaningless. Is IV of 18% high or low for Tata Consultancy Services Ltd? Depends on the historical range. If the past year's range is 14%-28%, 18% is below the midpoint — relatively low. If the range is 12%-20%, 18% is near the high — relatively high. The same absolute number means completely different things in different historical contexts.

How to use historical IV for TCS

Look at the IV chart over a 1-year window and mentally note the high, low, and midpoint. Today's value is then interpretable relative to this range. Above the midpoint = elevated. Below = depressed. Near the high = extreme. Near the low = extreme (opposite direction). This interpretation is the foundation of every IV-based strategy decision on TCS.

Different lookback periods on TCS

Different lookback periods give different pictures. 30-day lookback shows short-term context. 1-year lookback shows long-term context. 6-month lookback is a middle ground. For positional trades, prefer longer lookbacks. For day trades, shorter lookbacks are more responsive. The Tata Consultancy Services Ltd IV chart should support switching between these periods.

Using historical IV for trade decisions on TCS as of 15 July 2026

Before any IV-dependent trade, check where current IV sits in the historical range. Only sell premium when IV is high in the context you care about. Only buy when it is low. Never ignore context. This single discipline differentiates consistently profitable option traders from those who blindly trade based on today's absolute numbers.

Tata Consultancy Services Ltd (TCS) IV Chart: Avoiding Common Mistakes

Mistake 1: buying options at high IV

The most expensive mistake in options trading is buying at high IV. You pay an inflated premium, and even correct direction often fails to produce profit because IV crushes against you. Always check the Tata Consultancy Services Ltd IV chart before buying any option. If IV is in the top quartile, find another way to express your view — directional futures, spreads, or waiting.

Mistake 2: selling options at low IV

The opposite mistake — selling premium when IV is low — means you collect thin premium with unlimited tail risk. The risk-reward is terrible. Only sell premium when IV compensates you for the risk. The IV chart helps you avoid these trades by showing clearly when premium is rich enough.

Mistake 3: ignoring upcoming events

Tata Consultancy Services Ltd IV trades very differently around events. An elevated IV before an event is not necessarily expensive — it is priced for the expected post-event move. Selling it exposes you to the full event risk. Buying it exposes you to IV crush. Know the event calendar and adjust your IV interpretation accordingly.

Mistake 4: using IV without context on TCS as of 15 July 2026

IV values without historical context are meaningless. An IV of 16% might be high, low, or normal depending on Tata Consultancy Services Ltd's recent range. Always compare today to the past 30-90 days before drawing conclusions. Without this context, you are guessing, not analysing.

IV Chart: Video Walkthrough

TCS IV Rank & IV Percentile: quick reference

| IVR / IVP band | Premium regime | Common strategy bias |

|---|---|---|

| Below 20% | Very cheap options | Buy premium — long straddles, strangles, debit spreads |

| 20% – 40% | Below-average IV | Lean buyer; prefer debit spreads over selling thin premium |

| 40% – 60% | Fair-value zone | No volatility edge; trade TCS direction, not vol |

| 60% – 80% | Elevated premium | Sell premium — credit spreads, iron condors |

| Above 80% | Extreme / event-driven IV | Rich premium, but check the event calendar before selling |

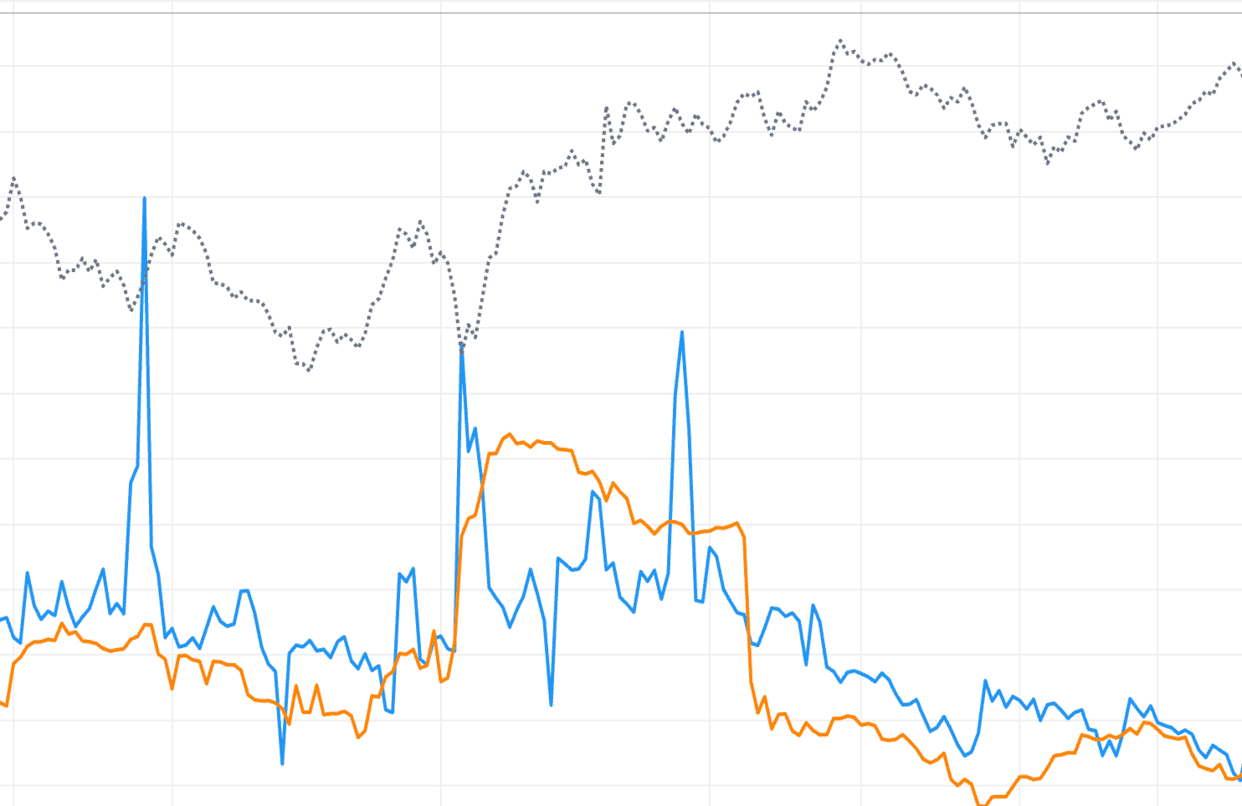

These bands are conventions used by NSE premium sellers, not fixed rules — ahead of a scheduled event a high IVR reading is normal and can persist until the event resolves. The live TCS chart above plots IVR and IVP against your chosen lookback, so you can see in real time which regime current option pricing sits in.

How to use the StockMojo IV Chart

- Select an underlying — Choose Nifty, BankNifty, or any F&O stock from the symbol selector.

- Read the current IV reading — The chart shows IV plotted over time. Note the latest value and where it sits relative to the visible range.

- Check IV Rank and IV Percentile — Look at the IV Rank and IV Percentile metrics displayed beside the chart. Values above 50% suggest elevated IV; below 50% suggest depressed IV.

- Compare IV vs HV — Toggle the historical volatility overlay. A wide gap (IV well above HV) signals overpriced options; a narrow or inverted gap signals underpriced options.

- Pick your strategy bias — Use the IV regime to bias toward premium selling (high IV) or premium buying (low IV) before entering a trade.

TCS IV Chart — Frequently Asked Questions

What is TCS implied volatility (IV)?

TCS implied volatility (IV) is the market's forward-looking estimate of how much TCS will move, derived by solving an option pricing model backwards from live NSE option premiums. High IV means options are expensive and a big move is priced in; low IV means options are cheap. IV measures expected magnitude of movement, not direction.

What is a good IV Rank (IVR) for selling TCS options?

An IV Rank above 50% is the common filter for selling TCS premium, and above 75% is a strong sell-side setup. IVR scales current IV between its 52-week low (0%) and high (100%), so a high reading means options are rich versus the past year. Below 25%, premium is cheap and buying strategies are favoured instead.

What is the difference between IV, HV and RV on the TCS chart?

IV is the forward-looking volatility implied by current TCS option prices, HV (historical volatility) measures actual movement over a past window, and RV (realised volatility) tracks what price is doing right now. When IV trades well above HV, TCS options are overpriced relative to real movement — an edge for premium sellers; a narrow or inverted gap favours buyers.

What causes an IV crush in TCS options?

IV crush is the rapid collapse of implied volatility once a scheduled event resolves the uncertainty that was inflating it. For TCS, common triggers are RBI policy meetings, the Union Budget, election results, quarterly earnings and major global data. Premiums deflate within minutes even when the direction was right, so option buyers avoid entering at pre-event IV peaks.

How often does the TCS IV chart update?

During NSE market hours (9:15 AM to 3:30 PM IST) the TCS IV chart refreshes every minute, recomputing IV from live option premiums alongside HV, RV and the futures price. IVP and IVR are recalculated against your selected lookback (default 252 sessions). Outside market hours the chart shows the last traded session's readings.