RELIANCE IV vs HV Chart | Volatility Premium & Discount Analysis

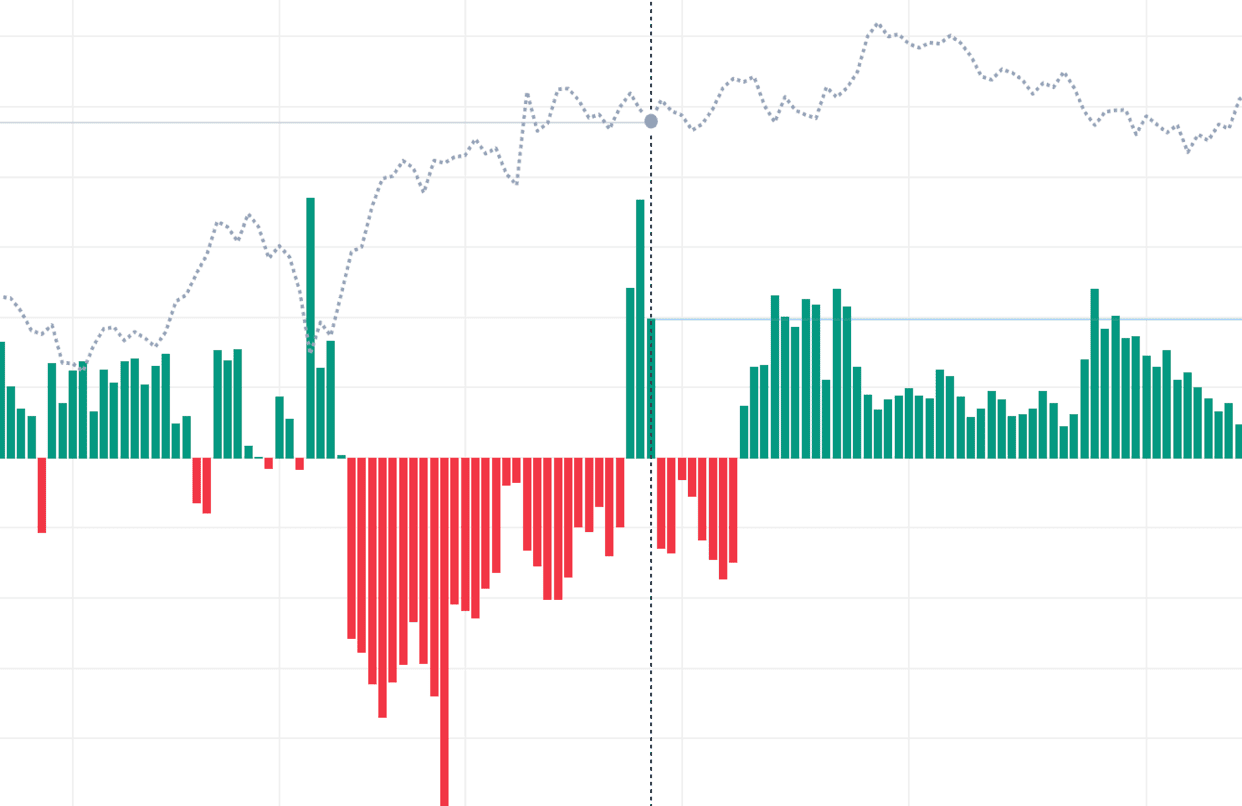

IV vs HV for RELIANCE is the cleanest way to tell whether options on this underlying are cheap or expensive at any moment. Implied volatility (IV) is the volatility number baked into current RELIANCE option prices — what the market expects going forward. Historical volatility (HV) is the actual standard deviation of past RELIANCE returns over a chosen window — what the stock has actually done. The gap between the two tells you whether option buyers are over- or under-paying relative to recent reality.

When RELIANCE IV is meaningfully above HV, the option market is pricing in more volatility than has actually been realized — premium is rich, and strategies like selling strangles, short straddles, and iron condors have favourable math. When IV drops below HV, option premium is cheap relative to the moves RELIANCE has been making, and long-volatility strategies (long straddles, backspreads) get interesting. The ratio also reveals regime changes: a sustained IV-HV premium collapse often precedes breakouts, while expanding IV-HV premium usually marks complacency ahead of events.

Practical use of RELIANCE IV-HV on NSE F&O

Most systematic option-selling strategies on RELIANCE should filter entries by IV-HV gap — entering short-premium trades only when IV is sufficiently above HV compensates for the inherent tail risk. For event-day trades (budget, RBI, expiry), comparing current RELIANCE IV with the HV you'd expect during the event window helps you decide whether the implied move is realistic, optimistic, or conservative — a crucial input for sizing and strike selection.

Combine IV vs HV with our IV Chart, Volatility Skew, and ATM Straddle Chart for a full RELIANCE volatility analysis stack on NSE.

Reliance Industries Ltd (RELIANCE) IV vs HV: Understanding the Difference

What is HV for RELIANCE?

Historical Volatility (HV) measures how much Reliance Industries Ltd (RELIANCE) has actually moved in the recent past. It is calculated from actual price changes over a chosen period — typically 20 or 30 days. HV is backward-looking and objective. It tells you what the market DID, not what it expects.

What is IV for RELIANCE?

Implied Volatility (IV) is the market's forecast of future volatility, derived from current option premiums. It is forward-looking and subjective — based on what traders collectively expect, not what has already happened. The IV vs HV chart plots both values over time so you can compare expectation against reality.

Why compare the two for RELIANCE?

The comparison reveals whether options are overpriced or underpriced relative to actual movement. If IV is much higher than HV, options are expensive — the market expects more future movement than it has been seeing. If IV is below HV, options are cheap — the market expects less. These mismatches create trading opportunities for informed Reliance Industries Ltd traders.

Using the chart today

As of 17 July 2026, open the RELIANCE IV vs HV chart and check the current spread. IV meaningfully above HV suggests selling premium. IV below HV suggests buying. A small spread (IV ≈ HV) means options are fairly priced and directional analysis matters more than IV-based trades.

Reliance Industries Ltd (RELIANCE) IV-HV: Spotting Volatility Regime Changes

What is a volatility regime on RELIANCE?

A volatility regime is the general state of volatility — compressed, normal, or elevated. Reliance Industries Ltd spends most time in normal or compressed regimes with occasional shifts to elevated. The IV-HV chart reveals the regime because both measures together show whether volatility is low, high, or average compared to history.

Compressed regimes on RELIANCE

In compressed regimes, both IV and HV are low. The IV-HV chart shows both lines near the bottom of their historical range. These regimes often precede volatility spikes because complacency breeds unexpected shocks. Short premium trades work but can be blindsided by sudden regime changes.

Elevated regimes on RELIANCE

In elevated regimes, both IV and HV are high. The chart shows both lines near the top of their range. These regimes often follow shocks and persist until calm returns. Long premium strategies may work but risk is high. Generally, elevated regimes favor defensive positioning over aggressive directional bets.

Transitions between regimes as of 17 July 2026

Watch the IV-HV chart for signs of transition. Rising HV signals a new elevated regime may be starting. Falling HV signals a return to compression. These transitions are the most important points for Reliance Industries Ltd traders because they change which strategies work best. Adjust your playbook when you spot a regime change.

Reliance Industries Ltd (RELIANCE) IV-HV: Reading Extreme Readings

What counts as an extreme reading on RELIANCE?

Extreme readings are IV-HV spreads that are significantly above or below the recent 3-6 month range. For Reliance Industries Ltd, spreads above 10 percentage points or below 0 are typically extreme. These extremes are rare and represent the highest-conviction trade setups because mean reversion is most powerful when the starting point is extreme.

Trading extreme high spreads on RELIANCE

When the spread is extremely high, the mean-reversion setup for short premium is strongest. Sell premium with modest size (remember, extremes can go further). Target profit as the spread compresses 50-70%. Exit if the spread widens further beyond a predefined threshold — your thesis may be wrong.

Trading extreme low spreads on RELIANCE

When the spread is extremely low (IV below HV), buying premium has an edge. Long straddles or directional options benefit from IV catching up to HV. The challenge is that low-IV environments often persist longer than expected because of calm markets. Use modest size and be patient for the reversion.

Risk at extremes as of 17 July 2026

Extreme readings are high-conviction setups but not risk-free. The biggest losses often come from "contagion" events that break the mean-reversion pattern. Always size trades so that the worst case is survivable. For Reliance Industries Ltd, extreme IV-HV readings appear a few times per year — being selective on the best ones beats trying to trade every one.

IV vs HV: Video Walkthrough

RELIANCE IV-HV spread: quick reference

| IV minus HV (vol points) | Premium regime | Common reading |

|---|---|---|

| Below 0 | Volatility discount | Rare; options cheap vs realized moves — long straddles and backspreads favoured |

| 0 – 2 | Thin premium | Quiet regime on RELIANCE; little edge for either side |

| 2 – 5 | Normal risk premium | Standard short-premium zone — strangles, iron condors, credit spreads |

| 5 – 10 | Event-inflated premium | Market pricing an event (results, RBI, budget); rich premium but real move risk |

| Above 10 | Extreme premium | Typical pre-earnings on stocks; expect IV crush once the event passes |

These bands are typical NSE tendencies, not fixed rules — indices usually hold a smaller IV-HV spread than single stocks, and spreads widen ahead of scheduled events. The live RELIANCE chart above plots IV minus HV each session, so you can see which regime the option market is pricing right now and how today compares with recent history.

How to use the IV vs HV chart

- Pick an underlying — Select Nifty, BankNifty, or an F&O stock to compare implied versus historical volatility for.

- Compare the lines — IV is the forward-looking line; HV is the backward-looking line. Look at the current vertical gap between them.

- Evaluate the spread — A positive spread (IV > HV) favours premium-selling. A negative or near-zero spread favours premium-buying or long-volatility strategies.

- Check historical context — Scan how the spread has behaved over recent months. Is today's spread normal for this stock, or an outlier?

- Pick a strategy — Elevated IV-HV spread → short strangles, iron condors, credit spreads. Compressed IV-HV → long straddles, backspreads, debit spreads.

RELIANCE IV vs HV — Frequently Asked Questions

What is RELIANCE IV vs HV?

RELIANCE IV (Implied Volatility) is the volatility priced into current option premiums — the market's forward expectation. HV (Historical Volatility) is the annualised standard deviation of actual past RELIANCE returns over a chosen window. When IV is above HV, options are relatively expensive; when IV is below HV, option premium is cheap versus realized movement.

How to trade RELIANCE using IV vs HV?

Use the RELIANCE IV-HV spread as a strategy filter. When IV is well above HV, premium is rich — selling structures like short strangles and iron condors have favourable expected value. When IV drops to or below HV, premium is cheap — long straddles and backspreads become attractive. Always confirm with price action and upcoming events before entering.

Does RELIANCE IV move before HV?

Yes. IV reacts the moment expectations change because it is derived from live RELIANCE option prices, while HV only updates as new daily returns enter its rolling window, so it lags by several sessions. An IV spike ahead of an event is therefore a leading signal — by the time HV catches up, the move has usually already happened.

What is a normal IV-HV spread for RELIANCE?

Most NSE underlyings, including RELIANCE, trade with IV about 1-3 percentage points above HV — a normal volatility risk premium. A spread above 5 points usually signals event anticipation (results, budget, RBI policy) and tends to revert once the event passes. IV falling below HV is rare and marks unusually cheap option premium.

How often does the RELIANCE IV vs HV chart update?

During NSE market hours (9:15 AM to 3:30 PM IST) the RELIANCE IV line refreshes from the live option chain, while HV is recalculated from daily closing returns over your selected window (21 sessions by default). Outside market hours the chart shows the last traded session, and the historical series lets you study past spread behaviour.