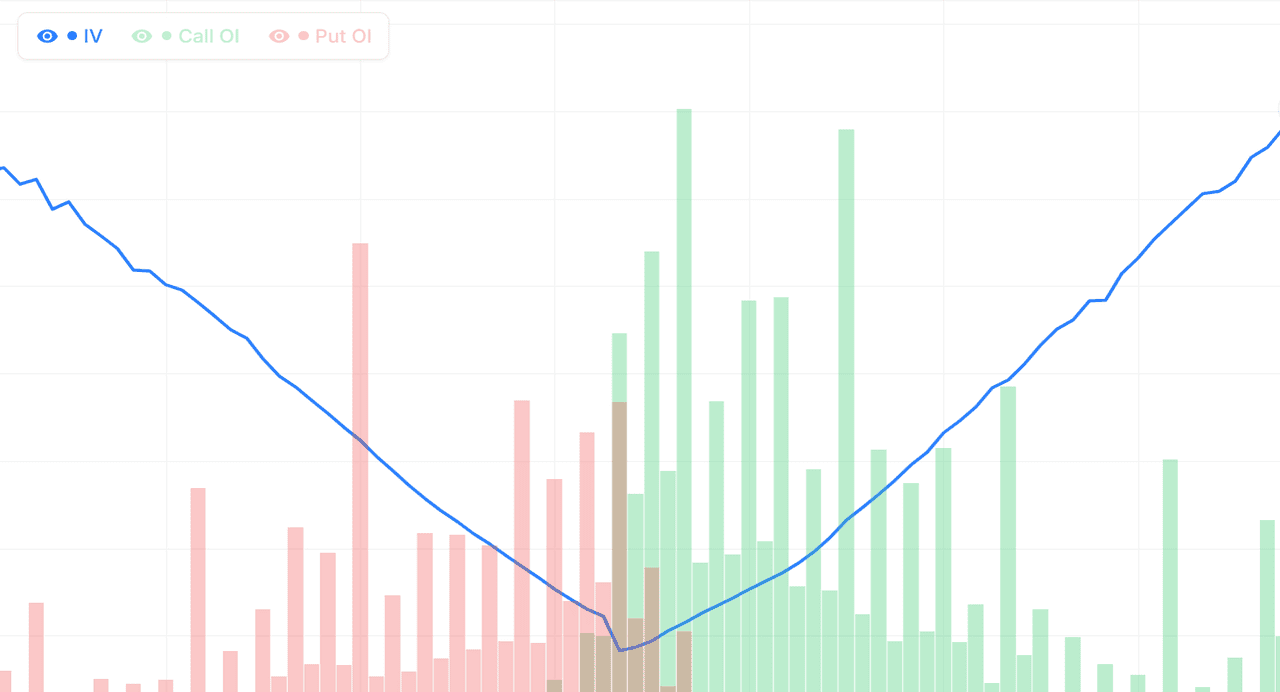

FINNIFTY Volatility Skew & Smile | Live IV Distribution

Implied volatility across FINNIFTY option strikes is almost never flat — it forms a characteristic smile or skew shape that reflects how the market prices tail risk. Our volatility skew tool plots IV at every strike for each FINNIFTY expiry, so you can see at a glance whether out-of-the-money puts are trading at a premium (the classic downside skew typical of Indian indices), whether the smile is flat (complacent market), or whether calls are unusually expensive (a sign of buy-side demand and potential squeeze risk).

The FINNIFTY IV surface is a richer read. By comparing skew across the near, mid, and far expiries, you can tell whether the market is pricing event-specific risk (skew spikes only in the relevant expiry) or structural fear (skew is elevated across all expiries). A steepening skew in FINNIFTY during an up-move often signals that sophisticated traders are buying protection against a reversal, while a flattening skew during a sell-off tells you downside hedges are being unwound — often an early sign of a bottom.

Trading FINNIFTY with volatility skew

Premium-selling strategies on FINNIFTY benefit from trading the rich side of the skew — for example, selling the overpriced FINNIFTY OTM puts when downside skew is unusually steep, or selling expensive calls when the smile is flipped. Risk-reversal structures (long call, short put or vice versa) let you isolate and trade the skew itself rather than direction. For directional traders, a sudden flattening of skew alongside a price rally is a textbook confirmation of a sustained move. Live mode streams skew updates through each NSE session.

Combine volatility skew with our IV Chart, IV Grid Screener, and ATM Straddle Chart for comprehensive FINNIFTY implied volatility analysis.

Nifty Financial Services (FINNIFTY) Volatility Smile vs Smirk Explained

What is the volatility smile pattern on FINNIFTY?

The volatility smile pattern occurs when implied volatility is elevated for both deep OTM puts AND deep OTM calls, with the ATM strike showing the lowest IV. The chart looks like a U — a smile shape. This pattern appears when the market expects significant moves in either direction but is uncertain about which way. On Nifty Financial Services, smiles are less common than smirks but do appear around major uncertainty events where both upside and downside are plausible.

What is the volatility smirk on FINNIFTY?

The smirk is asymmetric — IV is much higher on one side than the other. The most common pattern on FINNIFTY is a put smirk: OTM puts have significantly higher IV than OTM calls. This reflects equity-market reality — investors fear downside crashes more than they fear missing upside. The smirk is the default shape you will see on most trading days for Nifty Financial Services, and reading its steepness tells you how much fear is priced in.

When does the FINNIFTY smirk become a smile?

A smile emerges when far-OTM calls also become expensive — both tails are pricing in risk. This happens in rare situations: speculative rally markets where traders chase upside, before binary events with unclear outcomes, or during extreme uncertainty periods. If you see the Nifty Financial Services skew transitioning from a smirk to a smile, something unusual is happening. Investigate why before making large directional trades.

Inverted skew patterns on FINNIFTY

Occasionally, OTM calls become more expensive than OTM puts — the opposite of the normal pattern. This is called an inverted skew. It usually happens during strong speculative rallies (early-stage meme-style buying), before bullish events with perceived upside bias, or in specific stocks during takeover rumours. Inverted skews are uncommon for index options but do appear in stock options. As of 15 July 2026, if you see FINNIFTY with an inverted skew, check what news or event is driving the unusual pattern.

Nifty Financial Services (FINNIFTY) Skew: Trading Strategies

Strategy 1: Sell expensive FINNIFTY OTM puts

When the Nifty Financial Services put skew is steep, OTM puts are expensive in IV terms. Selling them to collect the inflated premium is a classic skew trade. You profit if FINNIFTY stays above the put strike (premium decay) and suffer if it falls through. Size positions small because of tail risk. Manage by setting a stop-loss at a specific FINNIFTY price below the sold strike. The strategy works best when skew has been elevated for several sessions and you expect normalisation.

Strategy 2: Vertical spreads capturing FINNIFTY skew

Vertical spreads let you exploit the skew with limited risk. For a bear put spread: buy an ATM put (lower IV) and sell an OTM put (higher IV). You pay the IV differential but gain a position that profits if Nifty Financial Services declines. The skew reduces your net cost compared to spreads on symbols without put skew. Bear call spreads work the opposite way — sell an ATM call and buy an OTM call. Both strategies exploit the fact that option prices depend on IV, and skew creates mispricings.

Strategy 3: FINNIFTY calendar spreads with skew

Calendar spreads sell near-term and buy far-term options at the same strike. The skew affects this by influencing which strikes work best. Because near-term IV is often elevated when fear is high, selling near-term at high IV and buying far-term at lower IV captures both the time decay and the IV normalisation. For Nifty Financial Services, this approach works best during pre-event periods when the front-month skew is steeper than the back-month skew.

Strategy 4: FINNIFTY skew filters for other trades

You do not need to trade skew directly to benefit from skew analysis. Use it as a filter for other trades. If you are considering a long call position, check whether call IV is unusually high (bad entry point) or normal (reasonable entry). If you are considering a long put, check whether put IV is elevated (you are overpaying) or normal. The skew chart answers these questions in seconds. As of 15 July 2026, this filter approach fits most trading styles without requiring dedicated skew strategies.

Nifty Financial Services (FINNIFTY) Skew: Weekly and Monthly Differences

How does the FINNIFTY weekly skew differ from monthly?

Nifty Financial Services weekly options typically have slightly steeper skews than monthly options. The reason is time — weekly options have less time for price to move, so extreme moves are perceived as more shocking. This makes put protection in the short term relatively more expensive. When comparing weekly vs monthly skews, adjust your expectations for this natural difference.

When weekly FINNIFTY skew is much steeper than monthly

If the weekly skew is significantly steeper than the monthly (say, 12 points vs 6 points), near-term fear is elevated but medium-term concern is not. This usually happens before specific events in the near term — a data release, an RBI meeting, earnings. The weekly fear is event-specific while the monthly reflects the longer-term view. Trades can be structured around this difference.

When monthly FINNIFTY skew is steeper than weekly

Occasionally the monthly skew is steeper than the weekly. This is less common and often signals broader concerns that extend beyond the immediate timeframe. Maybe a major event is months away, or structural risks are being priced in. This pattern suggests patience is warranted — the market expects fear to last.

Cross-expiry skew trades on FINNIFTY

When skews differ significantly across expiries, calendar spreads can exploit the difference. Sell the steep-skew expiry (captures more premium) and buy the flatter-skew expiry (cheaper protection). This diagonal structure benefits from the normalisation of the skew differential. For Nifty Financial Services, this is an advanced technique that requires understanding of both time decay and skew dynamics. As of 15 July 2026, it works best during event-driven periods when skews diverge sharply.

Volatility Skew: Video Walkthrough

FINNIFTY volatility skew shapes: quick reference

| Skew shape | IV pattern across strikes | Positioning read |

|---|---|---|

| Steep put skew | OTM puts far above calls | Heavy downside hedging; fear rising; contrarian top risk at extremes |

| Mild put skew (normal) | OTM puts modestly above calls | Healthy FINNIFTY baseline; routine protection demand |

| Flat skew | Puts ≈ calls, curve nearly level | Complacency; low hedging demand; often a late-stage rally |

| Volatility smile | Both OTM wings above ATM IV | Two-sided tail risk; common around FINNIFTY events or results |

| Call-side (reverse) skew | OTM calls out-price puts | Speculative upside or squeeze demand; rare on indices |

On NSE indices a mild-to-steep put skew is the resting state, so the signal is in the change: a skew that steepens into a rally warns of hedging before a top, while one that flattens into a sell-off often marks capitulation near a bottom. Compare today's FINNIFTY curve against the T-day overlay above to judge whether the current shape is stretched.

How to read the Volatility Skew chart

- Select symbol and expiry — Choose Nifty, BankNifty, or any F&O stock and pick a weekly or monthly expiry.

- Identify the skew direction — Check whether IV is higher on the put side (downside skew, common for indices) or call side (upside skew, common in momentum stocks).

- Compare versus history — Toggle historical T-day overlay to see whether today's skew is unusually steep or flat versus the past 5 sessions.

- Spot the lowest-IV strike — Locate where IV bottoms. This is the market's implied forward price and the natural ATM reference.

- Pick your strategy bias — Use steep skew for premium-selling (sell the rich side), flat skew for long-volatility plays, and skew transitions for directional entries.

FINNIFTY Volatility Skew — Frequently Asked Questions

What is FINNIFTY volatility skew?

Volatility skew is the pattern of implied volatility plotted across strike prices for one FINNIFTY expiry. In theory IV should be flat; in practice it slopes. FINNIFTY options usually show put skew — out-of-the-money puts price at higher IV than equidistant calls — because traders pay up for downside protection.

Why do FINNIFTY options usually show a put skew?

Put skew reflects structural hedging demand. Funds and institutions holding FINNIFTY exposure continuously buy out-of-the-money puts to protect portfolios, lifting put-side IV above call-side IV. Index sell-offs are also faster and sharper than rallies, so puts carry a permanent risk premium. Even in strong uptrends the FINNIFTY put skew rarely disappears — it only flattens.

What does a steepening FINNIFTY volatility skew mean?

A steepening skew means out-of-the-money FINNIFTY put IV is rising faster than call IV, so hedging demand and fear are increasing. It often appears while spot is still climbing, marking sophisticated desks buying protection before a reversal. At extremes steep put skew is a contrarian caution signal that a pullback may be near.

What does flat or call-side skew tell me on FINNIFTY?

A flat FINNIFTY skew signals complacency — puts and calls price at similar IV, meaning little hedging demand and often a late-stage rally. Call-side or reverse skew, where OTM calls out-price puts, points to speculative upside demand or squeeze risk. Both are unusual for indices and worth watching as sentiment extremes.

How often does the FINNIFTY volatility skew chart update?

During NSE market hours (9:15 AM to 3:30 PM IST) the FINNIFTY volatility skew chart refreshes every minute from live option-chain IV across strikes. Outside market hours it shows the last traded session, and historical mode lets you replay the FINNIFTY skew curve for any past expiry to study how it behaved around events.